Estimating Total Accident Costs

Safety committees should promote the idea that substantial savings in estimated future accident costs may be realized if management approves the recommendation. To do that, cite cost estimates for the accident cited in the report, and use that total as a baseline estimate for future savings if a similar accident occurs. Include two categories of accident costs in the recommendation: insured-direct costs and uninsured-indirect costs.

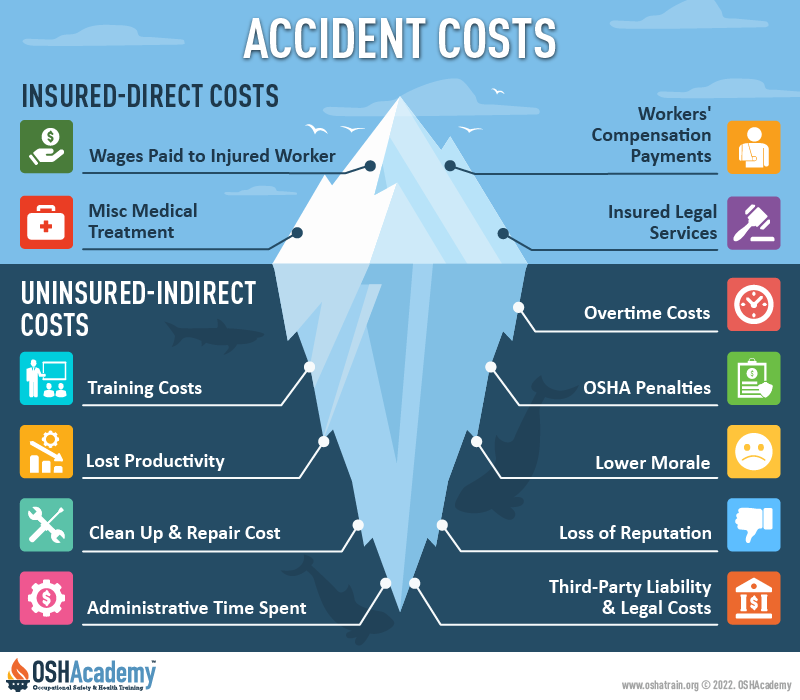

- Insured-direct costs: These costs are usually covered by insurance premiums. They represent just the "tip of the iceberg."

- Uninsured-indirect costs: These are the underlying costs the employer pays for, usually "out of pocket," for consequences not covered by insured-direct costs. They represent the part of the iceberg under water that you don't see, and like the iceberg, the cost are always greater.

Click below to see a list of examples of direct and indirect costs.

Direct-insured costs include:

- injured worker's wages during injury

- workers' compensation payments

- medical treatment expenses

- costs for insured legal services

Uninsured-indirect costs include:

- Wages paid to injured workers for absences not covered by workers' compensation.

- Cost of wages related to time lost through work stoppage associated with the worker injury.

- Overtime costs necessitated by the injury.

- Administrative time spent by supervisors, safety personnel, and clerical workers after an injury.

- Training/retraining costs for a replacement worker.

- Lost productivity related to work rescheduling, new employee learning curves, and accommodation of injured employees.

- Damaged equipment and materials clean-up, repair, and replacement.

- Costs of accident investigations.

- OSHA fines and any associated legal action.

- Employer-paid medical, third-party liability, and legal costs.

- Worker pain and suffering.

- Loss of reputation and goodwill from bad publicity.

The indirect costs for accidents will usually be greater than the direct costs. Indirect costs can range from 1 to 20 times greater than the direct costs, depending on the total costs of the injury. For every $1 spent in direct costs, you’ll pay an additional $1 to $6 in indirect costs. You can estimate the ratio based on accident costs by visiting OSHA's Individual Injury Estimator: Background of Cost Estimates webpage.

Let's say an employee fractured his leg while working around the machinery in our scenario. If the total accident costs are $100,000 (indirect cost = $50,000 and the direct cost = $50,000), the ratio between indirect and direct costs based on the OSHA Injury Estimator will be 1 to 1.

So, now the question is, how much will the employer save in the future by investing now? We'll answer that question in the next section.

Knowledge Check Choose the best answer for the question.

7-6. What can safety committees use to best emphasize the savings the company may realize if they approve a recommendation?

You forgot to answer the question!